OCTOBER 6, 2022

Fannie Mae Joins Freddie, FHA to Use Rent Payments

By Talis Shelbourne

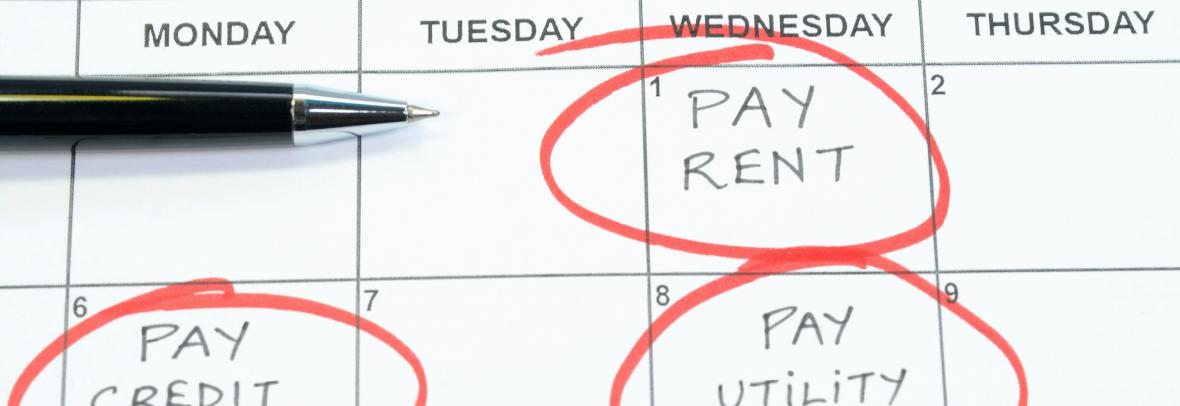

A majority of mortgage providers will now allow renters with thin credit scores to include on-time rent payments in the data a lender uses when considering approvals.

WASHINGTON – Fannie Mae launched its Multifamily Positive Rent Payment Reporting pilot program last week, offering a national lifeline to aspiring homeowners with no established credit history.

The program is expected to have a significant impact on cities with high renter populations and on groups that often have difficulty establishing credit.

Fannie Mae, officially the Federal National Mortgage Association, was created by Congress during the Great Depression. The public-private “government-supported enterprise” purchases mortgages from financial institutions.

Fannie Mae had already updated its computer-automated system last year to include bank records showing consistent rent payments by individuals. The system, called the Desktop Underwriter, is used by lenders to evaluate the creditworthiness of mortgage applicants.

The change meant individuals could collect documentation of their rent payments made via check, electronically through a rental management’s payment portal and through other electronic methods connected to a bank and provide those to a mortgage lender as evidence of a good rental history. Freddie Mac and FHA loans previously announced rent-payment considerations.

This latest rent reporting program allows the renters of multifamily properties to report their rent payment history. As an incentive, Fannie Mae will cover the first year of costs associated with reporting that data.

According to Fannie Mae, if a renter misses a payment, they are automatically unenrolled so it does not damage their credit score; landlords, however, are allowed to report missed rent payments to credit agencies on their own, which would negatively impact credit history.

Credit is an essential part of the home buying process, and experts advise prospective homeowners achieve a credit score of at least 620 to get the best rates for a mortgage.

The lender ultimately decides to approve the loan. In some cases, Fannie Mae will purchase a loan to “guarantee” it, which means it is responsible for the debt if the borrower defaults.

© 2022 Journal Media Group.

![Myths About Today’s Housing Market [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/04/21104919/20220422-MEM-1046x1690.png)