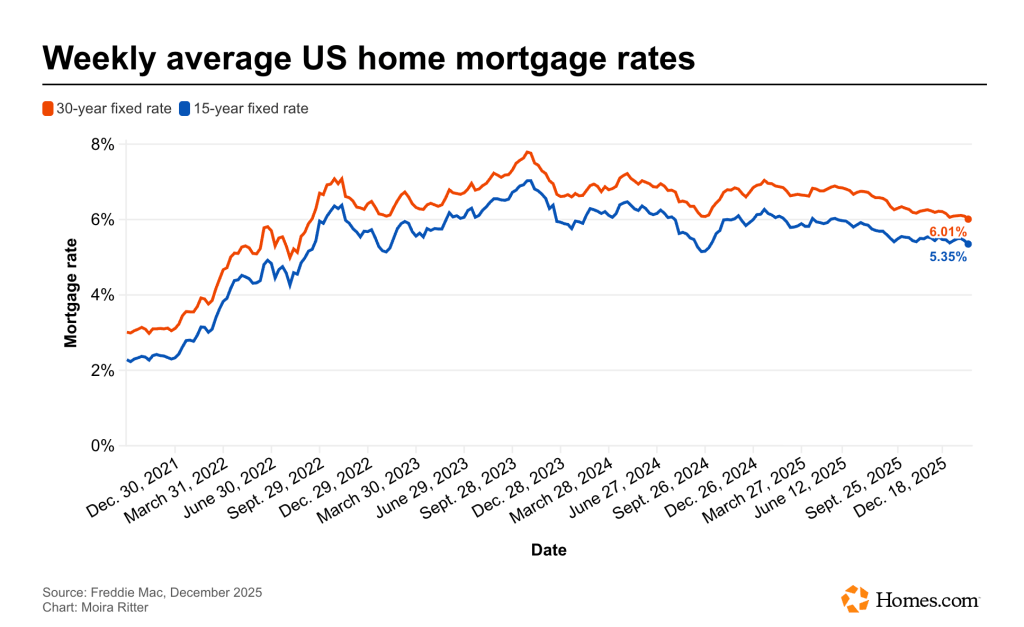

The 30-year, fixed-rate stood at 6.01% as of Thursday

By Moira Ritter -Homes.com

February 19, 2026

Key takeaways

- Mortgage rates fell to their lowest averages since September 2022, with the 30-year fixed at 6.01% and the 15-year at 5.35%.

- Lower rates have fueled a sharp increase in refinancing, but home sales and pending contracts remain weak amid affordability challenges and winter conditions.

- Economists expect spring to bring more buyer activity, with millions of households newly able to qualify for a mortgage at today’s rates.

Mortgage rates are at their lowest averages since September 2022.

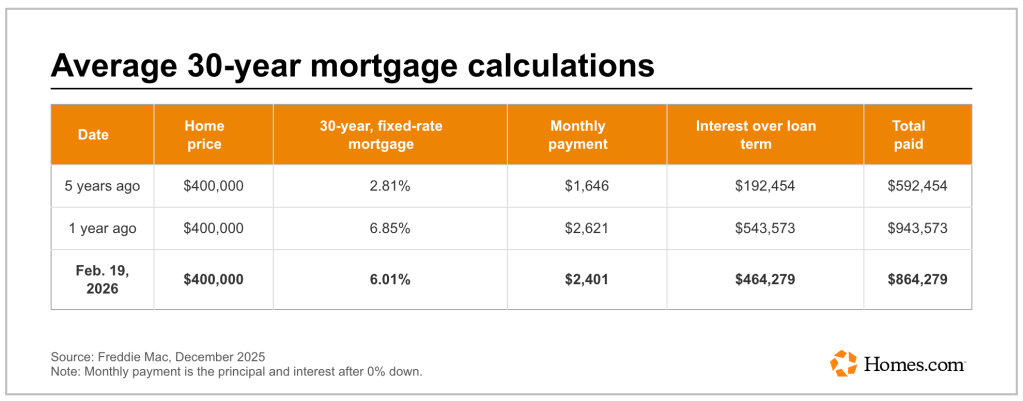

As of Thursday, the 30-year, fixed-rate mortgage averaged 6.01%, according to mortgage giant Freddie Mac. It’s the second consecutive week of declines. This time last year, the average was 6.85%.

The 15-year, fixed-rate mortgage also saw a drop in the week ended Thursday, averaging 5.35%. That’s down from last week’s average (5.44%) rate and last year’s (6.04%).

On a daily basis, mortgage rates were unchanged, according to Mortgage News Daily. The 30-year, fixed-rate mortgage was at 6.05%, and the 15-year, fixed-rate mortgage stood at 5.62% as of Thursday afternoon.

Lower mortgage rates could bring more buyers back to the market

The recent downward shift in mortgage rates has yet to translate to a shift in home sales, but experts are hopeful that the spring market — and weather — will bring at least a little more activity.

Applications for home purchases, for example, are higher than a year ago, but on a weekly basis they’ve been more volatile, according to data from the Mortgage Bankers Association. Refinance demand, however, has been on the upswing.

“This lower rate environment is not only improving affordability for prospective homebuyers, it’s also strengthening the financial position of homeowners,” Sam Khater, chief economist at Freddie Mac, said in a statement Thursday. “Over the past year, refinance application activity has more than doubled, enabling many recent buyers to reduce their annual mortgage payments by thousands of dollars.”

At the same time, the National Association of Realtors’ latest existing and pending home sales reports have been lackluster. In December, sales of pre-owned homes fell 8.4%, the sharpest monthly drop in roughly four years.

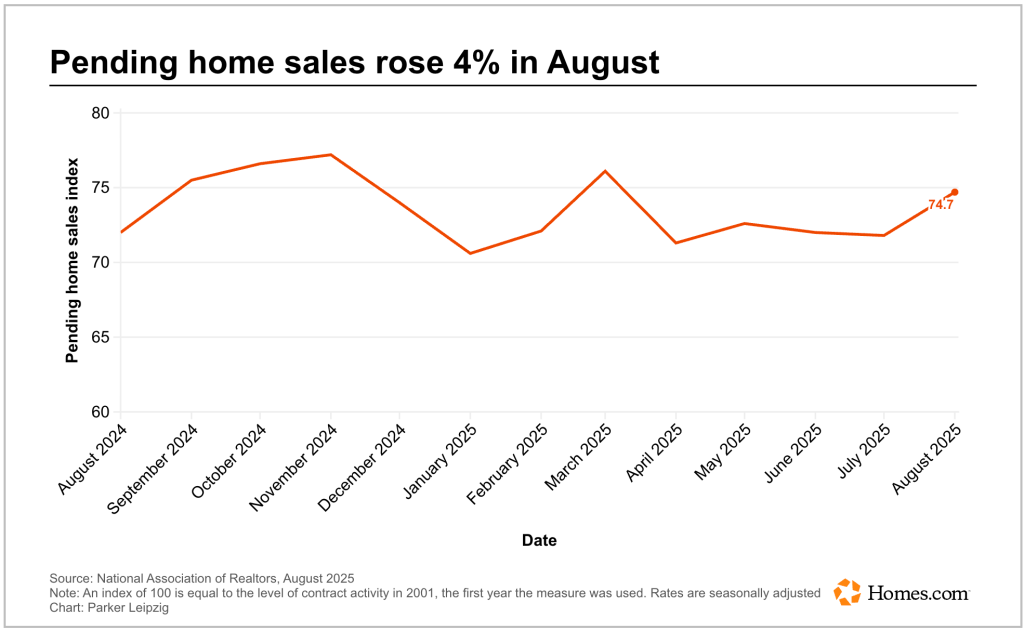

On Thursday, the association reported that pending home sales — the number of signed contracts for single-family houses, townhouses, condominiums and co-ops — declined in January on both a monthly and annual basis. The report is considered a leading indicator for where the market and buyer demand are headed.

Taken together, the data reflects a slow market driven by buyers hampered by affordability barriers — or winter weather.

Even so, there’s optimism that the spring could bring more activity, especially with the expected seasonal influx of inventory. Lawrence Yun, chief economist at the NAR, noted that an additional 5.5 million households that couldn’t afford a mortgage last year could now qualify at today’s lower rates.

“Most newly qualifying households do not act immediately, but based on past experience, about 10% could enter the market — potentially adding roughly 550,000 new homebuyers this year compared with last year,” he said in a statement Thursday.