Share of homeowners with rates above 6% has overtaken those under 3%

By David Holtzman – Homes.com

January 14, 2026

The housing market recently reached a milestone that suggests the “lock-in” effect, discouraging home sellers from putting their properties on the market, is slowly on its way out.

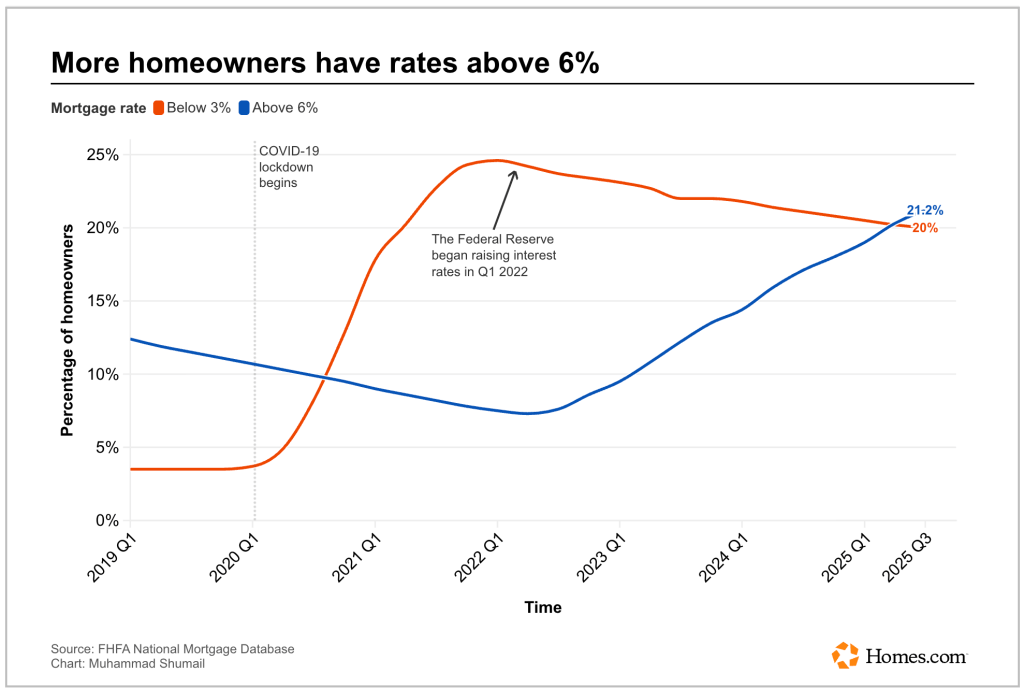

In the second half of 2025, more homeowners had mortgages with rates at or above 6% than those with loans below 3%, according to the Federal Housing Finance Agency. It was the first time this had been the case since late 2020, during the midst of the COVID-19 pandemic.

Since the first quarter of 2022, when the U.S. Federal Reserve began raising interest rates to counter the impact of rapidly escalating inflation, the share of homeowners with rates below 3% has been slowly declining.

From a peak of 24.6% in early 2022, the figure had fallen to 20% by the third quarter of 2025. Meanwhile, owners with rates at or above 6% climbed from 7.3% in mid-2022 to 21.2% late last year.

The pandemic is what led to the lock-in effect, a situation in which numerous owners have very low mortgage rates when the marketplace average is far higher. People who already own a house don’t want to sell and buy another property if it means they will lose their low rate. They are “locked in,” pressured to stay where they are rather than put their homes up for sale.

This phenomenon has been troublesome for the housing market, leading to a scarcity of existing homes for potential buyers already burdened by today’s much higher mortgage rates. The lack of available homes was one of the reasons why the median age of first-time homebuyers reached a record 40 years old in 2025, with existing owners staying in their houses much longer than in the past.

“The median expected tenure in a purchased home is now 15 years, with 28% of buyers declaring it’ll be their ‘forever home’ and that they never intend to move,” the National Association of Realtors reported in its 2025 Profile of Home Buyers and Sellers. “This marks a significant increase from 2000 to 2008 when sellers typically stayed in their homes for just six years.”

The lock-in effect has also posed problems for economic growth in general, as it means people are less likely to relocate for better job opportunities, according to a 2023 paper by Lu Liu, an assistant professor of financeat the University of Pennsylvania’s Wharton School.

Other factors motivate sellers

This trend, along with the slow decline in average mortgage rates for buyers, could motivate some people to get off the sidelines.

“This definitely boosts activity a little bit,” Steve Trautwein, senior loan officer for Intercoastal Mortgage LLC in Northern Virginia, told Homes.com. “It’s not world-changing, it’s not a big shot to the markets, “but it’s a meaningful step forward.”

What Trautwein has seen more in recent months is people who decide to sell because they need to move for a job or some other reason, rather than shifts in mortgage rates.

“I personally sold a house this summer with a [sub-3%] mortgage on it so the sellers could move to where they needed to be,” he said.

The largest share of outstanding mortgages currently, almost a third, falls within the range of 3% to 4%, according to the FHFA. Therefore, there are still many homeowners with rates significantly lower than the average 30-year rate, which was just over 6% last week.

“Eventually, more of those locked into low rates will be forced to move due to life cycle or financial reasons, bringing more inventory to the real estate market,” Melissa Cohn, regional vice president of William Raveis Mortgage, told Homes.com. “If mortgage rates were to decline into the mid-5s or lower, we would see more and more people willing to give up their low rates and make the move that they have been waiting to do.”