The housing market needs mortgage rates to decrease to help unwind the lock-in effect and thaw the supply of existing homes for sale, Fannie Mae said.

WASHINGTON — Single-family home prices nationally increased 5.8% from Q4 2023 to Q4 2024, an acceleration from the previous quarter’s downwardly revised annual growth rate of 5.4%, according to the latest reading of the Fannie Mae Home Price Index (FNM-HPI).

On a quarterly basis, home prices rose a seasonally adjusted 1.7% in Q4 2024, up from the downwardly revised 1.2% growth rate in Q3 2024. On a non-seasonally adjusted basis, home prices increased just 0.3% in Q4 2024. The FNM-HPI is a national, repeat-transaction home price index measuring the average, quarterly price change for all single-family properties in the United States, excluding condos.

“Year-over-year home price growth accelerated in the fourth quarter, following back-to-back quarters of deceleration,” said Mark Palim, Fannie Mae senior vice president and chief economist. “Inventories of existing homes for sale have improved from a year ago but remain historically low, due largely to the so-called ‘lock-in effect.’ Since the beginning of October, mortgage rates have rebounded after bottoming out around 6.1% and are now inching closer to a new psychological barrier, the 7% threshold. The higher mortgage rate environment is not only hurting affordability, but it’s also exacerbating the lock-in effect by further reducing homeowners’ incentive to move.”

Palim continued: “The housing market in 2025 faces a difficult balancing act, with a notable decline in mortgage rates likely needed to help unwind the lock-in effect and thaw the supply of existing homes for sale. However, we believe such a decline would likely jumpstart demand from potential first-time homebuyers currently waiting to purchase, which could lead demand to outpace any improvement in supply, further exacerbating already-high home prices and purchase affordability.”

Methodology: The FNM-HPI is produced by aggregating county-level data to create both seasonally adjusted and non-seasonally adjusted national indices that are representative of the whole country and designed to serve as indicators of general single-family home price trends. The FNM-HPI is publicly available at the national level as a quarterly series with a start date of Q1 1975 and extending to the most recent quarter, Q4 2024. Fannie Mae publishes the FNM-HPI approximately mid-month during the first month of each new quarter.

Curious about selling your home? Understanding how much equity you have is the first step to unlocking what you can afford when you move. And since home prices rose so much over the past few years, most people have much more equity than they may realize.

Here’s a deeper look at what you need to know if you’re ready to cash in on your investment and put your equity toward your next home.

Home Equity: What Is It and How Much Do You Have?

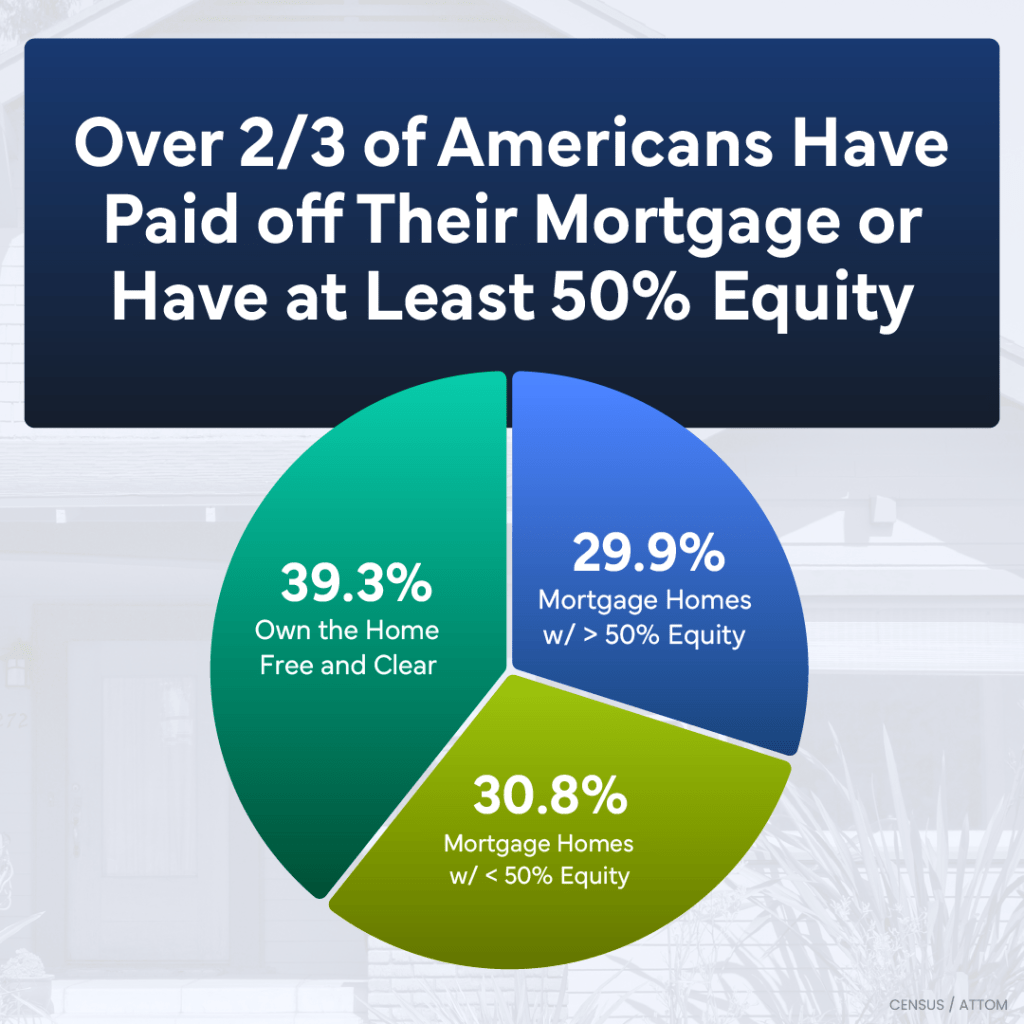

Home equity is the difference between how much your house is worth and how much you still owe on your mortgage. For example, if your house is worth $400,000 and you only owe $200,000 on your mortgage, your equity would be $200,000.

Recent data from the Census and ATTOM shows Americans have significant equity right now. In fact, more than two out of three homeowners have either completely paid off their mortgages (shown in green in the chart below) or have at least 50% equity in their homes (shown in blue in the chart below):

Today, more homeowners are getting a larger return on their homeownership investments when they sell. And if you have that much equity, it can be a powerful force to fuel your next move.

What You Should Do Next

If you’re thinking about selling your house, it’s important to know how much equity you have, as well as what that means for your home sale and your potential earnings. The best way to get a clear picture is to work with your agent, while also talking to a tax professional or financial advisor. A team of experts can help you understand your specific situation and guide you forward.

Bottom Line

Home prices have gone up, which means your equity probably has too. Let’s connect so you can find out how much you have in your home and move forward confidently when you sell.

For those looking for the good news about today’s real estate market. A bit of a deep dive, about 60 minutes worth but excellently delivered. Three main facts tell us it’s not all doom and gloom. Combine them with the time of year and the general fear that has most buyers/sellers on the sidelines, spells opportunity. (40:00). We can help should you decide to take advantage of today’s market.

Historical trends, what happens after quantitative tightening (12:00)

Demographics, there’s a lot of millennials (24:50)

Inventory levels, yes they are still historically low (22:00)

They now make up 45% of all homebuyers, up from 37% last year, even as affordability issues persist. Repeat buyers may have pulled back due to rising interest rates.

CHARLOTTE, N.C. – First-time home buyers have returned to the housing market, and those who can afford a home are finding success after years of setbacks. The share of buyers purchasing a home for the first time has rebounded to pre-pandemic levels.

First-time buyers now represent 45% of all buyers, up from 37% of buyers surveyed last year, according to Zillow’s 2022 Consumer Housing Trends Report. If they can overcome affordability challenges, first-time buyers could be well positioned to continue increasing their share in today’s shifting market, with more options and time to decide on the right home.

The share of first-time buyers plummeted during the pandemic amid rapidly rising home values and tough competition, even with high demand coming from the large millennial generation. Zillow research found younger, likely first-time shoppers were losing out to older, repeat buyers who were able to tap the equity in their existing homes and use cash to make a stronger offer. A Zillow survey found younger buyers were more likely to report losing to an all-cash buyer at least once, as was the case for 45% of Gen Z and 38% of millennial buyers, compared to 30% of all buyers.

“First-time buyers now appear to be making relative gains as high mortgage interest rates disproportionately encourage current homeowners to stay put,” said Zillow population scientist Manny Garcia. “The flow of homes into the market is slowing, suggesting homeowners are likely comparing their current low mortgage rate to today’s rates and deciding not to move. While rising mortgage rates are hurting affordability for all buyers, first-time buyers may be less deterred by higher rates because they’re comparing a monthly mortgage payment to what they’re paying in rent.”

First-time buyers are making up a larger share of a smaller pie. Newly pending home sales were down 29% in August, compared to a year prior, as buyers struggle to keep up with higher home prices and interest rates. Home values remain 14.1% higher than last year, even after two consecutive month-over-month declines. When combined with rising mortgage interest rates, the typical monthly payment on a home is nearly 60% higher today than it was a year ago.

Recent Zillow research finds those affordability challenges have driven up demand for the lowest-priced homes in each market. While there are fewer buyers overall, first-time buyers may find more competition for starter homes.

The silver lining is that today’s much-needed market rebalancing has the potential to especially benefit first-time buyers, who have the flexibility to shop without trying to time the purchase of their new home with the sale of an existing home. Listings typically lingered 16 days on the market in August before going under contract, compared to eight days in June, meaning buyers have twice as much time to decide on a home compared to this time last year.

First-time buyers may also have more bargaining power as a growing number of sellers drop their prices. The share of listings with a price cut grew to roughly 28% in August, according to Zillow’s latest monthly market report.

As the market changes, aspiring first-time buyers may need to change their approach. These five tips are a good starting point:

Understand what’s affordable. As mortgage interest rates fluctuate, aspiring buyers can start with a mortgage calculator to understand what they can realistically afford on a monthly basis. Take into account some of the hidden costs of homeownership, such as property tax, insurance and HOA dues, which can add up to more than $750 per month. But it’s always best to leave some wiggle room in the budget for unexpected maintenance projects and emergency repairs. First-time shoppers should also explore down payment assistance programs they may qualify for.

Finance first. First-time buyers can gain a competitive edge by getting pre-approved for a mortgage. A Zillow survey finds 86% of sellers prefer a buyer who has been pre-approved, as opposed to pre-qualified, for a mortgage. This financial check gives sellers more certainty that a buyer will close on time, and it allows buyers to make a stronger, faster offer the minute the right home hits the market. Buyers can start the pre-approval process online. Don’t hesitate to try, try, try again. Nearly half of all first-time buyers (47%) are denied a mortgage at least once before ultimately getting approved.

Hire the right agent. An experienced agent will have a finger on the pulse of their local market and know all the changes happening in it, and they can help buyers make strategic decisions to win. They’ll know when to come in with an offer under list price or when to expect a bidding war. Buyers should plan on interviewing their top candidates and asking the right questions.

Shop smarter with tech. New real estate technology can help first-time buyers make faster, smarter decisions. Virtual 3D Home tours and interactive floor plans give shoppers a more authentic experience of a home, allowing them to quickly narrow down their options and tour fewer homes in person.

Keep the contingencies. With less competition, first-time buyers should have the leverage to include important contingencies in their offers that could potentially save them a lot of money in the long run. An inspection contingency can identify major structural, mechanical or safety issues that could be extremely costly to repair and cause buyer’s remorse. A financing or appraisal contingency will ensure a buyer can walk away with their earnest money if a home fails to be appraised for the offer price or if their financing falls through.