| The U.S. presidential election and FOMC meeting dominated headlines last week, while the housing market hummed along, continuing recent trends. Home prices, inventory levels, market pace, and new listing activity all saw similar annual trends as the previous week. Mortgage rates climbed to their highest level since April in the week, and are expected to continue higher as a result of postelection Treasury yields. The Fed meeting resulted in the anticipated 25 basis-point rate cut as the FOMC continues to make decisions based on incoming economic data. The coming months could bring more mortgage rate volatility as reactions to the election and its implications move through the market. Over the past year, the housing market has remained largely unaffordable to many would-be buyers. However, veteran borrowers can take advantage of the many benefits of a VA mortgage loan. Compared with the typical conforming mortgage loan, VA loans have more flexible credit criteria and lower mortgage rates; they even allow eligible borrowers to put down a lower down payment. Key findings The median listing price fell by 0.2% year over year The median listing price fell for the third week in a row. Home prices have hovered within a few percentage points of the previous year’s level since spring 2023. It is the 24th week in a row that the median listing price in the U.S. is less than or equal to what it was in the corresponding week of 2023. However, when a change in the mix of inventory toward smaller homes is accounted for, the median listing price per square foot increased by 1.7% this week compared with the same time last year. New listings—a measure of sellers putting homes up for sale—climbed 1.7% this week compared with one year ago The number of new listings on the market picked up compared with the same week last year. The recent upward trajectory of mortgage rates could largely discourage sellers from listing their homes as roughly 84% of outstanding mortgages have a rate of 6% or lower. Despite still-high rates, a recent read on home seller and buyer sentiment showed relatively rosy expectations. About 64% of sellers consider it a good time to sell, and just 22% of respondents expect mortgage rates to climb. Only time will tell whether the market will reflect this optimism. Active inventory increased, with for-sale homes 26.1% above year-ago levels For the 53rd consecutive week, the number of listings for sale has grown year over year. This week’s growth was lower than last week’s, the seventh week of slowing growth, and the lowest annual change since late March. Slowing listing activity and stifled buyer demand have resulted in slowing inventory growth. Downward progress in mortgage rates could stoke buyer demand, which could eat into the recent buildup in active inventory. Homes spent 9 days more on the market compared with this time last year The annual gap in time on the market increased to nine days this week, the biggest gap since July 2023. Generally, buyers have been holding off, waiting for more affordable housing conditions. However, with more options available, still-keen buyers might be feeling ready to act before winter. |

Mortgage Rates Ease, Ending 6-Week Climb

November 14, 2024

Mortgage Rates Ease, Ending 6-Week Climb

By Alex Veiga

Rates on 30-year mortgages slipped to 6.78% from 6.79% last week. Borrowing costs on 15-year fixed-rate mortgages fell to 5.99% from 6%.

NEW YORK — The average rate on a 30-year mortgage in the U.S. edged lower this week, ending a six-week climb.

The rate slipped to 6.78% from 6.79% last week, mortgage buyer Freddie Mac said Thursday. That’s still down from a year ago, when the rate averaged 7.4%.

Borrowing costs on 15-year fixed-rate mortgages, popular with homeowners seeking to refinance their home loan to a lower rate, also eased this week. The average rate slipped to 5.99% from 6% last week. A year ago, it averaged 6.76%, Freddie Mac said.

Mortgage rates are influenced by several factors, including the yield on U.S. 10-year Treasury bonds, which lenders use as a guide to price home loans. Bond yields have been rising in recent weeks following encouraging reports on inflation and the economy.

Last week, bond yields surged on expectations that President-elect Donald Trump’s plans to lower tax rates, increase tariffs and reduce regulation could ultimately lead to higher U.S. government debt and inflation, along with faster economic growth.

The yield on the 10-year Treasury was at 4.41% at midday Thursday. It was at 3.62% as recently as mid-September.

Despite its recent upward move, the average rate on a 30-year mortgage is still down from 7.22% in May, its peak so far this year. In late September, the average rate got as low as 6.08% — its lowest level in two years.

Economists predict that mortgage rates will remain volatile this year, but generally forecast them to hover around 6% in 2025.

Elevated mortgage rates and high prices have helped keep the U.S. housing market in a sales slump going back to 2022.

Copyright 2024 The Associated Press. All rights reserved. This material may not be published, broadcast, rewritten or redistributed without permission.

Highlights From the Profile of Home Buyers and Sellers

For most home buyers, the purchase of real estate is one of the largest financial transactions they will make. Buyers purchase a home not only for the desire to own a home of their own, but also because of changes in jobs, family situations, and the need for a smaller or larger living area. This annual survey conducted by the NATIONAL ASSOCIATION OF REALTORS® of recent home buyers.

Characteristics of Home Buyers

- First-time buyers decreased to 24% of the market share (32% last year). This year now marks the lowest share since NAR began collecting the data in 1981.

- The median first-time buyer age increased to 38 years old this year from 35 last year, while the typical repeat buyer age also increased to 61 years from 58 last year.

- 62% of recent buyers were married couples, 20% were single females, 8% were single males, and 6% were unmarried couples.

- 73% of recent buyers did not have a child under the age of 18 in their home. This is the highest share recorded.

- 17% of home buyers purchased a multigenerational home, for cost savings (36%), to take care of aging parents (25%), because of children or relatives over the age of 18 moving back home (21%, and children over the age of 18 who never left home (20%).

- 83% of buyers were White/Caucasian, 7% were Black/African-American, 6% were Hispanic/Latino, 4% were Asian/Pacific Islander, and 3% identified as some other race.

- 88% of recent home buyers identified as heterosexual, 3% as gay or lesbian, 2% as bisexual, 1% prefer to self-describe, and 6% preferred not to answer.

- 16% of recent home buyers were veterans and 2% were active-duty service members.

- At 22%, the primary reason for purchasing a home was the desire to own a home of their own. For first-time buyers, this number jumps to 64%.

Characteristics of Homes Purchased

- 15% of buyers purchased a new home, and 85% of buyers purchased a previously-owned home.

- Recent buyers who purchased new homes were most often looking to avoid renovations and problems with plumbing or electricity at 42%. Buyers who purchased previously-owned homes considered them a better value at 31%.

- Detached single-family homes continued to be the most common home type for recent buyers at 75%, followed by townhouses or row houses at 7%.

- Senior-related housing remained at 19% of buyers over the age of 60 this year. 58% purchased a detached single-family home, and 52% bought in a suburb or subdivision.

- The median distance between the home that recent buyers purchased and the home they moved from was 20 miles. This is down from the 2022 report of 50 miles but remains elevated from the distance of 15 miles seen from 2018 to 2021.

- Quality of the neighborhood (59%), convenience to friends and family (45%) and overall home affordability (36%) remained the most important factors to recent home buyers when choosing a neighborhood.

- Buyers typically purchased a home that was built in 1994. This is a rebound after the last two years, when buyers typically purchased a home built in the 1980s.

- Overall, buyers expected to live in their homes for a median of 15 years, while 25% said that they were never moving.

The Home Search Process

- In 2024, the home buying process for many started online, with 43% of buyers indicating that their first step was to look for properties on the internet. Additionally, 21% of buyers reached out to a real estate agent as their initial action.

- Real estate agents played a crucial role, with 86% of all buyers utilizing their services—the highest of all information sources used.

- Buyers spent a median of 10 weeks searching for a home in 2024, typically viewing seven homes, and two of those homes were viewed online only.

- All home buyers used the internet to search for a home. The most valuable content on websites were photos (41%), detailed information property information (39%), and floor plans (31%).

- 59% of recent buyers reported being very satisfied, and 33% expressed being somewhat satisfied with their recent home buying process.

Home Buying and Real Estate Professionals

- 88% of home purchases were made through a real estate agent or broker, demonstrating the continued importance of agents in the home buying process. 5% of buyers purchased directly from a builder or builder’s agent, and 5% purchased directly from the previous owner.

- Home buyers primarily sought help from an agent or broker in finding the right home to purchase (49%) and negotiating the terms of the sale (14%).

- 40% of buyers found their agent through a friend, neighbor, or relative. This trend was especially pronounced among first-time buyers, where 51% relied on referrals from their personal network.

- Most buyers only interviewed one agent before making a decision, with 77% of repeat buyers.

- 88% of home buyers would use their agent again or recommend to others.

Financing the Home Purchase

- 74% of all buyers financed their home purchase, a decrease from 80% last year. First-time buyers were more likely to finance their purchase at 91%, while only 69% of repeat buyers financed.

- 26% of home buyers paid cash for their home, an all-time high for all-cash buyers.

- 49% of recent home buyers used their savings to finance their home purchase, down from 54% last year. 25% of first-time buyers used a gift or loan from a relative or friend for their downpayment, though savings was most common at 69%.

- 52% of first-time buyers utilized a conventional loan to finance their home, 29% used an FHA loan, and 9% used a VA loan. The share of first-time buyers using an FHA loan has declined from 55% in 2009 to 29% in 2024.

- Buyers continue to see purchasing a home as a good financial investment. 79% reported believing that a home purchase is a good investment, and among those buyers, 39% said it was better than owning stocks.

Home Sellers and Their Selling Experience

- The typical age of home seller was 63 this year, the highest ever recorded.”

- For all sellers, the most commonly cited reason for selling their home was the desire to move closer to friends and family (23%), followed by home was too small (12%), home was too large (11%), and the neighborhood was becoming less desirable (10%).

- The median number of years a seller owned their home was 10 years, the same as last year. That number was higher than reported from 2000 to 2008, when the tenure in the home was only six years.

- 36% of sellers traded up and purchased a home that was larger in size than what they previously owned, 30% bought a home that was similar in size, and 32% traded down and purchased a home that was smaller in size.

- For recently sold homes, the final sales price was a median of 100% of the final listing price. This continues to be the highest recorded median since 2002.

- For all sellers, time on the market this year was a median of three weeks, one week longer than last year.

- 68% of sellers were very satisfied with the selling process. 22% were somewhat satisfied.

Home Selling and Real Estate Professionals

- 66% of recent sellers used an agent that was referred to them or used an agent they had worked with in the past to buy or sell a home.

- 81% of recent sellers contacted only one agent before finding the right agent they worked with to sell their home.

- 50% of sellers used the same real estate agent to represent them when purchasing or selling their home. That number jumps to 71% for sellers within 10 miles of their home purchase.

- Sellers place a high priority on the following three tasks: help market the home to potential buyers (22%), price the home competitively (20%), and sell the home within a specific timeframe (18%).

- The real estate agent’s reputation remains the most important factor when sellers select an agent to sell their home (35%), and an agent’s trustworthiness and honesty (21%).

- Most sellers—87%—said that they would definitely (72%) or probably (15%) recommend their agent for future services.

For-Sale-by-Owner (FSBO) Sellers

- 90% of sellers sold with the assistance of a real estate agent, up from 89% last year, and only 6% were FSBO sales. The share of FSBO sellers was a historical low.

- For 38% of all FSBO sellers, the main reason to sell via FSBO was because they sold to a relative, friend, or neighbor.

- Getting the price right (17%), selling within the length of time planned (13%), and understanding and performing the paperwork (10%) were the most difficult steps for FSBO sellers.

- FSBOs typically sell for less than the selling price of other homes; FSBO homes sold at a median of $380,000 in 2023 (up from 310,000 in 2022), still far lower than the median selling price of all homes, which was $435,000.

Why Now’s Not the Time To Take Your House Off the Market

Has your house been sitting on the market longer than expected? If so, you’re bound to be frustrated by now. Maybe you’re even thinking it’s time to pull the listing and wait to see what 2025 brings. But what you may not realize is, the decision to hold off could actually cost you. Here’s a look at why staying the course could be the smarter move.

Other Sellers Are Pulling Back. Should You Hold Off Too?

According to recent data from Altos Research, the number of withdrawals is increasing – that means more sellers are opting to pull their listings off the market right now. And this isn’t unusual for this time of the year.

In the housing market, there are seasonal ebbs and flows. Inventory levels typically start to drop off a bit headed into the fall season as some sellers delay their plans until the new year. As Mike Simonsen, Founder of Altos Research, explains:

“. . . we’re seeing a more normal seasonal pattern now with inventory beginning to decline. We’re also seeing more home sellers withdrawing their listings to try again next year. In fact, for every two sales, there is another listing withdrawn from the market.”

But is that a smart move? While it might seem like a good idea to pull your listing too, here’s why that approach may not pay off this year.

Today’s Buyers Are Serious and Ready To Act

The biggest reason to stick with your plan to sell now is that the buyers who are looking at this time of year are serious about making a purchase.

They’ve been sitting on the sidelines for a while waiting for affordability to improve. And now that mortgage rates are down from their recent peak, they’re ready to make their move. Mortgage applications are rising – and that’s a leading indicator that buyers are preparing to jump back in. And since they’ve already put their needs on the back burner for so long, they’re even more eager than buyers usually are at this time of year.

These aren’t window shoppers. They’re highly motivated buyers who want to move fast – and that’s the kind of buyer you want to work with. As Freddie Mac says:

“During the fall months, serious homebuyers are eager to settle in to a new home before the holiday season ramps up and the winter weather begins.”

By keeping your home on the market, you increase the chances of attracting people who are truly ready to make a purchase.

Bottom Line

While some sellers are choosing to take their homes off the market, this really isn’t the best move. With serious buyers eager to purchase, this is a great time to sell your house. Let’s connect to make sure we’ve got a strategy in place to make it happen.

Local Real Estate Insights: Impact on Home Prices

If you’re wondering what’s going on with home prices lately, you’re definitely not the only one. With so much information out there, it can be hard to figure out your next move.

As a buyer, you might be worried about paying more than you should. And if you’re thinking of selling, you might be concerned about not getting the price you’re aiming for.

So, here’s a quick breakdown to help clear things up and show you what’s really happening with prices—whether you’re thinking about buying or selling.

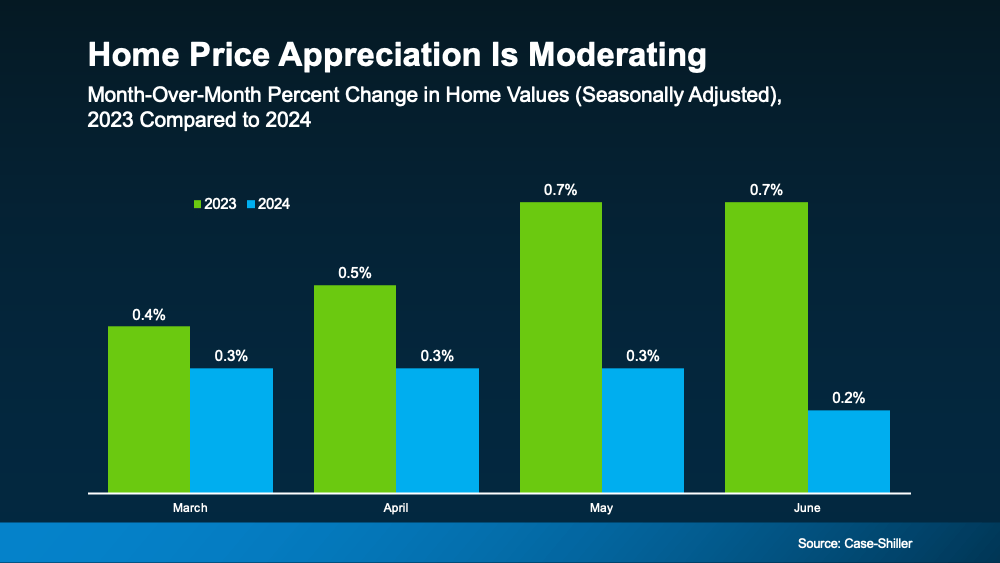

Home Price Growth Is Slowing, but Prices Aren’t Falling Nationally

Throughout the country, home price appreciation is moderating. What that means is, prices are still going up, but they’re not rising as quickly as they were in recent years. The graph below uses data from Case-Shiller to make the shift from 2023 to 2024 clear:

But rest assured, this doesn’t mean home prices are falling. In fact, all the bars in this graph show price growth. So, while you might hear talk of prices cooling, what that really means is they’re not climbing as fast as they were when they skyrocketed just a few years ago.

What’s Next for Home Prices? It’s All About Supply and Demand

You might be curious where prices will go from here. The answer depends on supply and demand, and it’s going to vary by local market.

Nationally, the number of homes for sale is going up, but there still aren’t enough of them to meet today’s buyer demand. That’s keeping upward pressure on prices – even though recent inventory growth has caused that home price appreciation to slow. Danielle Hale, Chief Economist at Realtor.com, said:

“. . . today’s low but quickly improving for-sale inventory has ushered in more market balance than would otherwise be expected . . . This should help home prices maintain a slower pace of growth.”

And here’s one other thing you may not have considered that could play a role in where prices go from here. Since experts say mortgage rates should continue to decline, it’s likely more buyers will re-enter the market in the months ahead. If demand picks back up, that could make prices climb a bit further.

Why You Should Work with a Local Real Estate Agent

While national trends give a big-picture view, real estate is always local – especially when it comes to prices. What’s happening in your neighborhood might be different from the national average based on what supply and demand look like in your market. That’s why it’s crucial to get local insights from a knowledgeable real estate agent.

As your go-to source for everything related to home prices, a local agent can provide the most current data and trends specific to your area.

So, if you’re planning to sell, they can help you price your house accurately. And when you’re ready to buy, they can find the right home that fits your budget and your needs.

Bottom Line

Home prices are still rising, just not as quickly as before. Whether you’re thinking about buying, selling, or just curious about what your house is worth, let’s connect so you have the personalized guidance you need.

Are We Heading into a Balanced Market?

If you’ve been keeping an eye on the housing market over the past couple of years, you know sellers have had the upper hand. But is that going to shift now that inventory is growing? Here’s a breakdown of what you need to know.

What Is a Balanced Market?

A balanced market is generally defined as a market with about a five-to-seven-month supply of homes available for sale. In this type of market, neither buyers nor sellers have a clear advantage. Prices tend to stabilize, and there’s a healthier number of homes to choose from. And after many years when sellers had all the leverage, a more balanced market would be a welcome sight for people looking to move. The question is – is that really where the market is headed?

After starting the year with a three-month supply of homes nationally, inventory has increased to four months. That may not sound like a lot, but it means the market is getting closer to balanced – even though it’s not quite there yet. It’s important to note this increase in inventory is not leading to an oversupply that would cause a crash. Even with the growth lately, there’s still nowhere near enough supply for that to happen.

The graph below uses data from the National Association of Realtors (NAR) to give you an idea of where inventory has been in the past, and where it’s at today:

For now, this is still seller’s market territory – it’s just not as frenzied of a seller’s market as it’s been over the past few years. As Mark Fleming, Chief Economist at First American, says:

“The faster housing supply increases, the more affordability improves and the strength of a seller’s market wanes.”

What This Means for You and Your Move

Here’s how this shift impacts you and the market conditions you’ll face when you move. Lawrence Yun, Chief Economist at NAR, explains:

“Homes are sitting on the market a bit longer, and sellers are receiving fewer offers. More buyers are insisting on home inspections and appraisals, and inventory is definitively rising on a national basis.”

The graphs below use the latest data from NAR and Realtor.com to help show examples of these changes:

Homes Are Sitting on the Market Longer: Since more homes are on the market, they’re not selling quite as fast. For buyers, this means you may have more time to find the right home. For sellers, it’s important to price your house right if you want it to sell. If you don’t, buyers might choose better-priced options.

Sellers Are Receiving Fewer Offers: As a seller, you might need to be more flexible and willing to compromise on price or terms to close the deal. For buyers, you could start to face less intense competition since you have more options to choose from.

Fewer Buyers Are Waiving Inspections: As a buyer, you have more negotiation power now. And that’s why fewer buyers are waiving inspections. For sellers, this means you need to be ready to negotiate and address repair requests to keep the sale moving forward.

How a Real Estate Agent Can Help

But this is just the national picture. The type of market you’re in is going to vary a lot based on how much inventory is available. So, lean on a local real estate agent for insight into how your area stacks up.

Whether you’re buying or selling, understanding how the market is changing gives you a big advantage. Your agent has the latest data and local insights, so you know exactly what’s happening and how to navigate it.

Bottom Line

The real estate market is always changing, and it’s important to stay informed. Whether you’re buying or selling, understanding this shift toward a balanced market can help. If you have any questions or need expert advice, don’t hesitate to reach out.

The Number One Mistake Sellers Are Making: Overpricing Their House

In today’s housing market, many sellers are making a critical mistake: overpricing their houses. This common error can lead to a home sitting on the market for a long time without any offers. And when that happens, the homeowner may have to drop their asking price to try to re-ignite buyer interest.

Data from Realtor.com shows the number of homeowners realizing this mistake and doing a price reduction is climbing (see graph below):

If you’re thinking about making a move yourself, here’s what you need to know. The best way to avoid making a costly mistake is to work with a trusted real estate agent to find the right price. Here’s a look at what’s at stake if you don’t.

Not Paying Attention To Current Market Conditions

Understanding current market conditions is key to accurate pricing. You don’t want to set your asking price based on what happened during the pandemic. The market has moderated a lot since then, so it’s far better to align your price with today’s reality.

Real estate agents stay updated on market trends and how they impact the pricing strategy for your house.

Pricing It Based on What You Want To Make (Not What It’s Worth)

Another misstep is pricing it based on what you want to make on the sale, and not necessarily current market value. You may see other homes in your neighborhood selling for top dollar and assume yours can do the same. But you may not be considering differences in size, condition, and features. For example, maybe that other house is waterfront or has a finished basement. To sum it up, Bankrate explains:

“How do you find that sweet spot of pricing for profit but not overpricing? The expertise of your agent can be truly valuable here. A knowledgeable agent will understand fair market value in your area, how much your house is worth and how much you might reasonably expect to get for it in the current market.”

An agent will do a comparative market analysis (CMA) to make sure your house is compared with truly similar properties to get an accurate look at how it should be priced.

Pricing High to Leave Room for Negotiation

Another common, yet misguided strategy is to price your house high on purpose, so you have more room to negotiate down during the sale. But this can backfire. A price that seems too high often deters potential buyers from even considering the home. So rather than leaving room for negotiation, what you’ll actually be doing is turning buyers away. U.S. News Real Estate explains:

“You want to sell your house for top dollar, but be realistic about the value of the property and how buyers will see it. If you’ve overpriced your home, chances are you’ll eventually need to lower the number, but the peak period of activity that a new listing experiences is already gone.”

An agent can help you set a fair price that attracts buyers and encourages more competitive offers.

Bottom Line

Overpricing your home can have serious consequences. A knowledgeable real estate agent brings an objective perspective, in-depth market knowledge, and a strategic approach to pricing.

Let’s connect so you can avoid making a pricing mistake that’ll cost you.

What Every Homeowner Should Know About Their Equity

Curious about selling your home? Understanding how much equity you have is the first step to unlocking what you can afford when you move. And since home prices rose so much over the past few years, most people have much more equity than they may realize.

Here’s a deeper look at what you need to know if you’re ready to cash in on your investment and put your equity toward your next home.

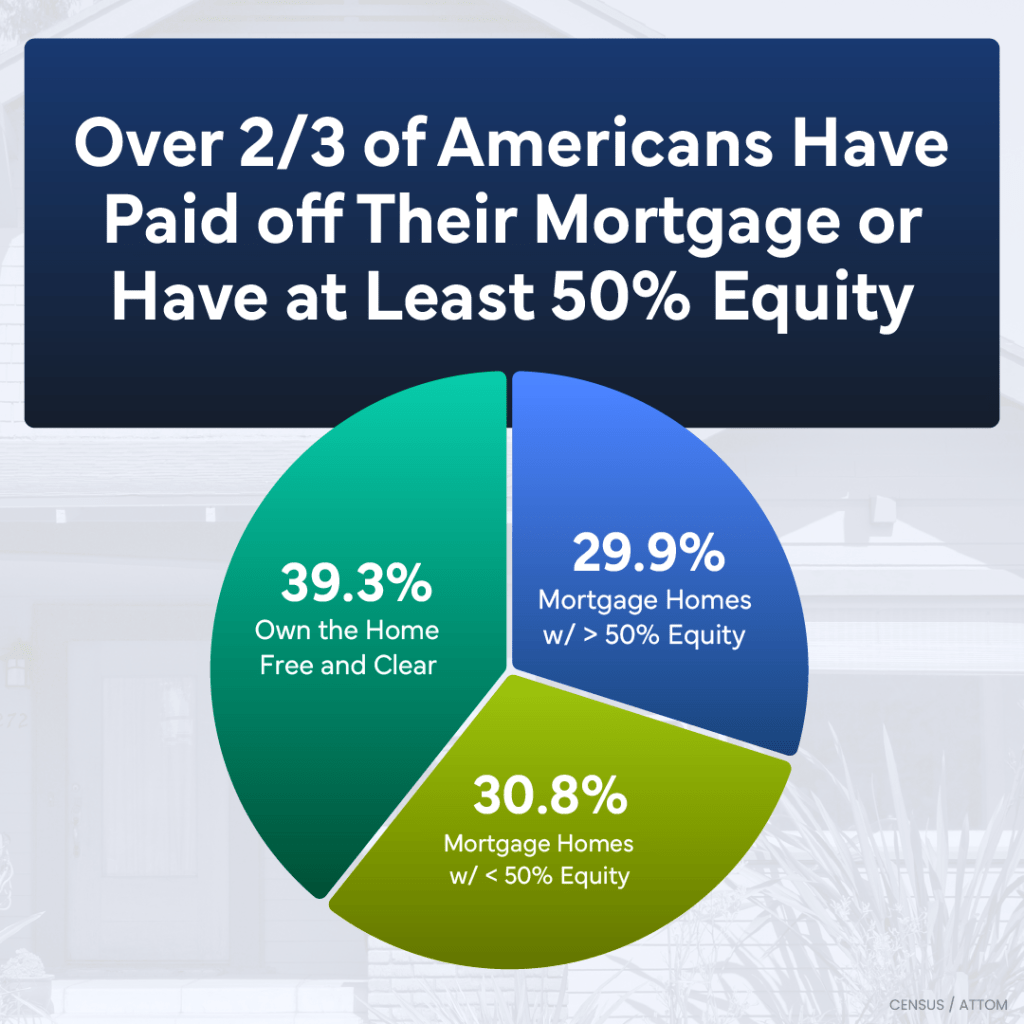

Home Equity: What Is It and How Much Do You Have?

Home equity is the difference between how much your house is worth and how much you still owe on your mortgage. For example, if your house is worth $400,000 and you only owe $200,000 on your mortgage, your equity would be $200,000.

Recent data from the Census and ATTOM shows Americans have significant equity right now. In fact, more than two out of three homeowners have either completely paid off their mortgages (shown in green in the chart below) or have at least 50% equity in their homes (shown in blue in the chart below):

Today, more homeowners are getting a larger return on their homeownership investments when they sell. And if you have that much equity, it can be a powerful force to fuel your next move.

What You Should Do Next

If you’re thinking about selling your house, it’s important to know how much equity you have, as well as what that means for your home sale and your potential earnings. The best way to get a clear picture is to work with your agent, while also talking to a tax professional or financial advisor. A team of experts can help you understand your specific situation and guide you forward.

Bottom Line

Home prices have gone up, which means your equity probably has too. Let’s connect so you can find out how much you have in your home and move forward confidently when you sell.

Nationally and some Florida Cities See Jump in Active Listings

courtneyk, iStock, Getty Images

MARCH 18, 2024

In Florida and nationwide, the housing supply is rebounding as sellers get used to elevated mortgage rates and the lock-in effect eases, Redfin found.

MIAMI – Active listings, or the total supply of homes for sale, in Cape Coral, North Port and Fort Lauderdale saw the biggest jump in the nation in February, the real estate brokerage firm Redfin reported. Nationwide, active listings climbed 0.8% from a month earlier on a seasonally adjusted basis and were little changed (-0.1%) from a year earlier — the smallest annual decline in months.

Nationally, new listings jumped 3.8% month over month on a seasonally adjusted basis in February to the highest level since September 2022. They were up 14.8% year over year, the largest annual gain since May 2021. In Florida, condo listings were the driving force contributing to the jump in supply amid a surge in HOA and insurance fees.

“The housing market is nothing like it was two years ago during the pandemic homebuying frenzy, but it’s better than it was last year. It’s coming back,” said David Palmer, a Redfin agent in Seattle. “Sellers who were on the fence in 2023 are now listing. They’re more used to elevated rates now. There still aren’t enough listings to quench pent-up buyer demand, but it’s getting better.”

Nationwide, housing supply is on the rise because the “lock-in effect” is easing; eventually, homeowners who have been holding on to their ultra-low mortgage rates simply have to move.

“February was a mixed bag for the housing market and the economy,” said Redfin Economics Research Lead Chen Zhao. “Housing supply is finally starting to recover in a meaningful way, which is great news for buyers who for months have been competing for a tiny pool of homes for sale. Still, many house hunters are hesitant to pull the trigger because mortgage rates and home prices remain elevated.”

Mortgage-purchase applications slid in February as mortgage rates ticked back up after dropping in December. The average 30-year-fixed mortgage rate was 6.78% in February up from 6.64% in January.

At the same time, prices continue to rise because, despite the recent uptick in listings, there’s still not enough supply to meet demand, Redfin said. Both new listings and active listings remained far below pre-pandemic levels in February.

“If you price your home reasonably, buyers will show up. If you don’t, buyers will wait for you to drop the price,” Palmer said. “I recently listed an estate sale fixer upper for $550,000 and it got 14 offers, sold for $75,000 over the asking price and the buyer waived every contingency.”

© 2024 Florida Realtors®

Courtesy Fannie Mae

JANUARY 22, 2024

Fannie Mae: 2024 Mortgage Rates to Dip Below 6%

By Amy Connolly

“Overall, we expect 2024 to be a better year than 2023 for homebuyer affordability and the mortgage industry,” Fannie Mae’s chief economist said.

WASHINGTON – The housing market will begin a gradual return to a “more normal balance” in 2024, and mortgage rates are expected to end the year below 6%, Fannie Mae analysts said.

Fannie Mae’s Economic and Strategic Research (ESR) Group said the lower rate environment should boost refinance volumes, which are already on the upswing. Lower rates are also likely to loosen the so-called lock-in effect that’s had a stronghold on the market.

“In fact, the ESR Group expects the annualized pace of existing home sales to move up to 4.5 million units by the fourth quarter of 2024, compared to 3.8 million in Q4 2023,” Fannie Mae analysts said in the January report. “However, a full recovery to the pre-pandemic sales rate is expected to take years, as housing affordability remains stretched extremely thin by historical standards relative to household incomes.”

At the same time, housing supply shortages and affordability constraints will continue to bolster the market for new single-family homes, with 2024 starts and new home sales forecast to top 2023 levels.

The ESR Group also said home prices are expected to rise 3.2% over the year, compared to 7.1% in 2023. While the latest forecast continues to project a slowdown in economic growth in 2024, the ESR Group anticipates a brighter economic backdrop compared to previous months, replacing its call for a modest recession with positive-but-below-trend growth in 2024.

The ESR Group noted the rapid recent easing in financial conditions, the Federal Reserve’s December meeting and the solid, upward trend in real personal income growth in October and November as positive impulses for growth over the coming quarters. But, the group said, the economy still faces a higher-than-normal risk of recession.

“Inflation’s decline and the resultant Fed pivot to signaling future rate cuts rates lead us to believe that home sales and mortgage originations likely bottomed out in the second half of 2023 and that a gradual improvement is now underway,” Doug Duncan, Fannie Mae senior vice president and chief economist, said.

“We expect mortgage rates to dip below 6% by year-end 2024 and for homebuilders to continue to add new supply, both of which should aid affordability. Additionally, the decline in mortgage rates is likely to push refinancing volumes upward, along with some pickup in purchase financing. However, even at less than 6 percent, we think rates will still have a significant way to go in order to meaningfully reduce the ‘lock-in effect’ experienced by homeowners who refinanced or bought during the pandemic. Overall, we expect 2024 to be a better year than 2023 for homebuyer affordability and the mortgage industry.”

© 2024 Florida Realtors®