Lisa Sturtevant PhD Bright MLS, Housing Economist

Inventory is climbing, which has been welcome news for prospective homebuyers. However, the inventory picture is very different depending on where you are and the type of home you’re looking for.

According to data from realtor.com, at the end of May 2025, total inventory across the U.S. was at about 90% of the May 2019 level. But a very distinct pattern emerges when you look at inventory by metro area. Inventory levels surpass 2019 levels in southern metros in Florida, Texas, and Arizona as well as in Washington and Oregon in the Pacific Northwest. By contrast, inventory across the Midwest and Northeast, as well as in Southern California, remains below 2019 levels.

Mid-Atlantic inventory remains tight

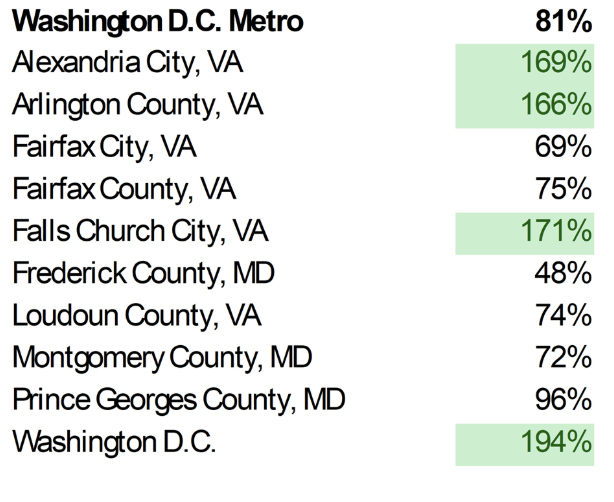

In the Bright MLS service area, which covers six states and the District of Columbia, there were 42,981 active listings on the market at the end of May 2025. The number of active listings is now 25.1% higher than it was a year ago and inventory has been increasing across the Mid-Atlantic region for 16 consecutive months, as more homes are listed for sale and properties remain on the market longer.

However, despite the rapid rise, inventory is still well below pre-pandemic levels in most local markets across the Bright MLS service area. Overall, May 2025 inventory is just 64% of the May 2019 level across Bright’s footprint. In fact, there are just a handful of counties in the region where inventory has surpassed 2019 levels.

The urban area housing markets tend to have more inventory. In both Philadelphia and Washington, D.C., inventory is above pre-pandemic levels. In the close-in suburbs of Arlington and Alexandria, Virginia, inventory has also surpassed what was available to buyers in 2019.

There are many more local markets where inventory is still less than half of what was available in 2019. In most of the Philadelphia suburbs, for example, the number of active listings in May 2025 is less than 50% of May 2019 levels.

So, while more inventory is a welcome change for homebuyers in the marketplace, inventory is still relatively tight across much of the Mid-Atlantic region and sellers do still have the upper hand in the market.