Contrary to the negative reports surrounding the market, people continue to move. Not everyone can or wants to wait. Job changes, growing families, downsizing, and other life events often dictate timing more than market trends. That’s why I start with the numbers. Not very exciting, I know but they’re essential. Understanding the data fosters informed decisions and an easier, less stressful path toward your unique real estate goals. I’m here to provide the numbers, break them down, demonstrate how they may affect you and guide you through the best way forward. DM me any time, and/or book a planning session.

U.S. house prices rose 4.8% year over year, from Jan. 2024 to Jan. 2025. For the nine census divisions, monthly home price changes ranged from -0.8% to +1%.

WASHINGTON — U.S. house prices rose 0.2% in January, according to the U.S. Federal Housing (FHFA) seasonally adjusted monthly House Price Index (FHFA HPI®). House prices rose 4.8% from January 2024 to January 2025. The previously reported 0.4% price growth in December was revised upward to 0.5%.

Among the nine census divisions, seasonally adjusted monthly home price changes ranged from a -0.8% in the South Atlantic division to +1.0% in the West North Central division. The 12-month changes were all positive, ranging from +2.4% in the West South Central division to +8.2% Middle Atlantic division.

The FHFA HPI is a comprehensive collection of publicly available house price indexes that measure changes in single-family home values based on data that extend back to the mid-1970s from all 50 states and over 400 American cities. It incorporates tens of millions of home sales and offers insights about house price changes at the national, census division, state, metro area, county, ZIP code, and census tract levels. FHFA uses a fully transparent methodology based upon a weighted, repeat-sales statistical technique to analyze house price transaction data.

FHFA releases HPI data and reports quarterly and monthly. The flagship FHFA HPI uses seasonally adjusted, purchase-only data from Fannie Mae and Freddie Mac. Additional indexes use other data, including refinances, mortgages insured by the Federal Housing Administration, and real property records. All the indexes (including their historic values) and information about future HPI release dates are available on FHFA’s website.

The next HPI report will be released April 29, 2025, and will include monthly data through February of 2025.

Danielle Hale, Chief Economist for Realtor.com March 7, 2025

Greater D.C. Area: Weekly Housing Market Update

Monitor the latest market activity in and around the nation’s capital with our experts’ week-by-week data breakdown. March 10, 2025 by Lisa Sturtevant, Phd

New listing activity rising seasonally in the D.C. region. The number of new listings coming on the market this past week is higher than last week, which is a typical seasonal trend. In the Washington D.C. region, new listings rose by 10.5% compared to last week. Across the overall Bright MLS service area, new listings were up 10.9% week-to-week. Early March tends to be the time of the year when prospective sellers are getting set to list in anticipation of the spring housing market.

Listings are still relatively higher in the Washington D.C. region though it is still too early to tell the extent to which DOGE is impacting homeowners.A total of 2,050 new listings came onto the market across the greater Washington D.C. region last week, which was 20.5% higher than the same week a year ago. Listings were up just 14.3% year-over-year in the broader Bright MLS footprint. If D.C. area homeowners were selling because they were impacted by federal government layoffs or back-to-the office mandates, we will continue to see relatively higher listing activity in the region in the weeks to come.

The Southern Maryland market may be one to watch. In Calvert County and Charles County in Maryland, new listing activity spiked this week. While it’s not possible to attribute this activity to federal government workforce changes, this market is one to watch. About one in five workers living in Calvert and Charles counties is a civilian federal government worker, according to data from the 2023 American Community Survey. In addition, these Southern Maryland communities attracted a lot of homebuying activity during the pandemic, including many workers who were able to work remotely at the time and may now be called back to the office.

Buyers are still out in the Washington D.C. region. There were 1,600 new pending contracts on homes in the D.C. region last week, a 12.1% increase compared to a week ago. This is a stronger week-to-week gain than we see in the broader Bright MLS service area and is a testament to the on-going demand within the area’s housing market. Places with more listing activity—for example, Calvert and Charles counties—saw some of the strongest uptick in new pending contract activity, as buyers took advantage of the increased availability of homes for sale.

Most states and metro areas saw home price growth last year. Prices increased more in areas with tighter inventory.

WASHINGTON – U.S. house prices rose 4.5% between the fourth quarter of 2023 and the fourth quarter of 2024, according to the Federal Housing Finance Agency House Price Index (FHFA HPI). House prices were up 1.4% compared to the third quarter of 2024. FHFA’s seasonally adjusted monthly index for December was up 0.4% from November.

“U.S. house prices grew at a slightly higher rate in the fourth quarter after three straight previous quarters of weaker appreciation,” said Dr. Anju Vajja, deputy director for FHFA’s Division of Research and Statistics. “The price growth accelerated during the quarter as the inventory of homes for sale tightened even further.”

Significant Findings

Nationally, the U.S. housing market has experienced positive annual appreciation each quarter since the start of 2012.

House prices rose in 49 states between the fourth quarter of 2023 and the fourth quarter of 2024. The five states with the highest annual appreciation were 1) Connecticut, 8.3%; 2) New Jersey, 8.3%; 3) Wyoming, 8.3%; 4) Vermont, 8.1%; and 5) Rhode Island, 7.6%. House prices declined in Mississippi by 0.2%.

House prices rose in 92 of the 100 largest metropolitan areas over the previous four quarters. The annual price increase was the greatest in urban Honolulu, HI at 18.7%. The metropolitan area that experienced the most significant price decline was Cape Coral-Fort Myers, FL at 6.3%.

All nine census divisions had positive house price changes year-over-year. The Middle Atlantic division recorded the strongest appreciation, posting a 7.1% increase from the fourth quarter of 2023 to the fourth quarter of 2024. The West South Central division recorded the smallest four-quarter appreciation, at 2.3%.

The FHFA HPI is a comprehensive collection of publicly available house price indexes that measure changes in single-family home values based on data that extend back to the mid-1970s from all 50 states and over 400 American cities. It incorporates tens of millions of home sales and offers insights about house price changes at the national, census division, state, metro area, county, ZIP code and census tract levels. FHFA uses a fully transparent methodology based upon a weighted, repeat-sales statistical technique to analyze house price transaction data.

There’s no perfect time to buy a home – every market has trade-offs. If you’re ready and can afford it, lean on a pro to make the most of current trends.

NEW YORK — It’s easy to get caught up in the idea of waiting for the perfect moment to make your move — especially in today’s market. Maybe you’re holding out and hoping mortgage rates will drop, or that home prices will fall. But here’s what you need to realize: trying to time the market rarely works. And here’s why.

There is no perfect market

No matter when you buy, there’s always some benefit and some sort of trade-off — and that’s not a bad thing. That’s just the reality of it. If you’re not sure you buy into that, think back to the last five years in housing.

Just a few years ago, mortgage rates hit a historic low. To take advantage of that, a ton of buyers rushed to buy a home and lock in those lower rates. The side effect? With such a big increase in how many buyers were purchasing, the homes on the market were snapped up fast. And since that resulted in so few homes left for sale, bidding wars became the norm and home prices went through the roof. Those buyers got a great rate, but they had other things to contend with.

Now, with higher rates and higher prices, it’s more expensive to buy. You can’t argue that. But at the same time, the number of homes for sale is at the highest point in several years. That means you have more options to choose from and you’ll be less likely to find yourself in a pull-out-all-the-stops bidding war. Again, there are benefits and trade-offs in any market.

So, if you have a reason to move and can afford to do so, you’ve got to take advantage of the trends that work in your favor and lean on a pro to help you navigate the rest. As Bankrate says:

“The complexities of the current conditions mean that, now more than ever, it’s smart to lean on the guidance of an experienced local real estate agent. If you want to enter the housing market in 2025, whether as a buyer or a seller, let a pro lead the way for you.”

While achieving your goals may feel like an uphill battle in today’s complex market, it is doable. But you’ll need the help of a trusted real estate agent and a lender.

Your agent will help you explore creative solutions — like looking into different housing types (like smaller condos), considering homes that need a little elbow grease, or casting a wider net for your search area. And your lender will walk you through different loan options and down payment assistance programs, so you know what you need to do to make the numbers work for you. As Yahoo Finance says:

“Buying a house at a time when both mortgage rates and home prices are favorable is a challenge. You probably shouldn’t try to time the housing market … Buy when it makes sense for you personally.”

Bottom line

There’s no perfect time to move — every market has its pros and cons. The key is knowing how to make the most of the factors working in your favor. If you need to move and can afford to do it, let’s connect so you’ll have the guidance and tools to make it possible.

The housing market needs mortgage rates to decrease to help unwind the lock-in effect and thaw the supply of existing homes for sale, Fannie Mae said.

WASHINGTON — Single-family home prices nationally increased 5.8% from Q4 2023 to Q4 2024, an acceleration from the previous quarter’s downwardly revised annual growth rate of 5.4%, according to the latest reading of the Fannie Mae Home Price Index (FNM-HPI).

On a quarterly basis, home prices rose a seasonally adjusted 1.7% in Q4 2024, up from the downwardly revised 1.2% growth rate in Q3 2024. On a non-seasonally adjusted basis, home prices increased just 0.3% in Q4 2024. The FNM-HPI is a national, repeat-transaction home price index measuring the average, quarterly price change for all single-family properties in the United States, excluding condos.

“Year-over-year home price growth accelerated in the fourth quarter, following back-to-back quarters of deceleration,” said Mark Palim, Fannie Mae senior vice president and chief economist. “Inventories of existing homes for sale have improved from a year ago but remain historically low, due largely to the so-called ‘lock-in effect.’ Since the beginning of October, mortgage rates have rebounded after bottoming out around 6.1% and are now inching closer to a new psychological barrier, the 7% threshold. The higher mortgage rate environment is not only hurting affordability, but it’s also exacerbating the lock-in effect by further reducing homeowners’ incentive to move.”

Palim continued: “The housing market in 2025 faces a difficult balancing act, with a notable decline in mortgage rates likely needed to help unwind the lock-in effect and thaw the supply of existing homes for sale. However, we believe such a decline would likely jumpstart demand from potential first-time homebuyers currently waiting to purchase, which could lead demand to outpace any improvement in supply, further exacerbating already-high home prices and purchase affordability.”

Methodology: The FNM-HPI is produced by aggregating county-level data to create both seasonally adjusted and non-seasonally adjusted national indices that are representative of the whole country and designed to serve as indicators of general single-family home price trends. The FNM-HPI is publicly available at the national level as a quarterly series with a start date of Q1 1975 and extending to the most recent quarter, Q4 2024. Fannie Mae publishes the FNM-HPI approximately mid-month during the first month of each new quarter.

Economists forecast rates to decline modestly, and new home sales to grow in 2025. The Sun Belt, including Florida, will see strong housing activity.

WASHINGTON — Affordability and the so-called “lock-in effect” are expected to keep housing activity subdued in 2025, with existing home sales forecast to move only slightly upward from recent multi-decade lows, according to the December 2024 commentary from the Fannie Mae Economic and Strategic Research (ESR) Group. The broader economy is expected to remain on solid footing and expand at an above-trend pace through 2026 as it navigates elevated core inflationary pressures and heightened policy uncertainty.

As part of its latest outlook, Fannie Mae’s economists shared five predictions for the housing market in 2025. They expect:

Average mortgage rates will decline modestly but remain above 6%, with likely bouts of volatility.

Existing homes sales will remain near 30-year lows, but location matters.

New home sales will remain a bright spot in the housing market (where they can be built).

National home price growth will decelerate.

Multifamily housing will remain in a holding pattern.

“From an affordability perspective, we think 2025 will look a lot like 2024, with mortgage rates above 6%, home price growth easing from recent highs but staying positive, and supply remaining below pre-pandemic levels,” said Mark Palim, Fannie Mae senior vice president and chief economist. “Still, heightened mortgage rate volatility may present opportunities for would-be homebuyers to take advantage of temporary lows, and we may see stretches where housing activity is boosted by lower rates – but, on average, we expect mortgage rates to remain elevated and a hindrance to activity. While we think conditions on a national basis will remain challenging, we’re seeing meaningful regional differences in market conditions, and the homebuying experience – as the adage goes – will continue to be a local one.

For example, in the Sun Belt, where construction has been robust for a few years and homebuilders are targeting first-time homebuyers with some offerings, we expect to see relatively strong housing activity. By comparison, we’re not expecting to see the same in the supply-constrained Northeast. And while we foresee the current affordability crunch hampering activity through our forecast horizon, we expect nominal wage growth will outpace home price growth for the first time in more than a decade in 2025, slowly but surely providing some much-needed relief to potential homebuyers.”

The U.S. presidential election and FOMC meeting dominated headlines last week, while the housing market hummed along, continuing recent trends. Home prices, inventory levels, market pace, and new listing activity all saw similar annual trends as the previous week. Mortgage rates climbed to their highest level since April in the week, and are expected to continue higher as a result of postelection Treasury yields. The Fed meeting resulted in the anticipated 25 basis-point rate cut as the FOMC continues to make decisions based on incoming economic data. The coming months could bring more mortgage rate volatility as reactions to the election and its implications move through the market.

Over the past year, the housing market has remained largely unaffordable to many would-be buyers. However, veteran borrowers can take advantage of the many benefits of a VA mortgage loan. Compared with the typical conforming mortgage loan, VA loans have more flexible credit criteria and lower mortgage rates; they even allow eligible borrowers to put down a lower down payment.

Key findings The median listing price fell by 0.2% year over year

The median listing price fell for the third week in a row. Home prices have hovered within a few percentage points of the previous year’s level since spring 2023. It is the 24th week in a row that the median listing price in the U.S. is less than or equal to what it was in the corresponding week of 2023. However, when a change in the mix of inventory toward smaller homes is accounted for, the median listing price per square foot increased by 1.7% this week compared with the same time last year.

New listings—a measure of sellers putting homes up for sale—climbed 1.7% this week compared with one year ago The number of new listings on the market picked up compared with the same week last year. The recent upward trajectory of mortgage rates could largely discourage sellers from listing their homes as roughly 84% of outstanding mortgages have a rate of 6% or lower. Despite still-high rates, a recent read on home seller and buyer sentiment showed relatively rosy expectations. About 64% of sellers consider it a good time to sell, and just 22% of respondents expect mortgage rates to climb. Only time will tell whether the market will reflect this optimism.

Active inventory increased, with for-sale homes 26.1% above year-ago levels For the 53rd consecutive week, the number of listings for sale has grown year over year. This week’s growth was lower than last week’s, the seventh week of slowing growth, and the lowest annual change since late March. Slowing listing activity and stifled buyer demand have resulted in slowing inventory growth. Downward progress in mortgage rates could stoke buyer demand, which could eat into the recent buildup in active inventory.

Homes spent 9 days more on the market compared with this time last year The annual gap in time on the market increased to nine days this week, the biggest gap since July 2023. Generally, buyers have been holding off, waiting for more affordable housing conditions. However, with more options available, still-keen buyers might be feeling ready to act before winter.

Has your house been sitting on the market longer than expected? If so, you’re bound to be frustrated by now. Maybe you’re even thinking it’s time to pull the listing and wait to see what 2025 brings. But what you may not realize is, the decision to hold off could actually cost you. Here’s a look at why staying the course could be the smarter move.

Other Sellers Are Pulling Back. Should You Hold Off Too?

According to recent data from Altos Research, the number of withdrawals is increasing – that means more sellers are opting to pull their listings off the market right now. And this isn’t unusual for this time of the year.

In the housing market, there are seasonal ebbs and flows. Inventory levels typically start to drop off a bit headed into the fall season as some sellers delay their plans until the new year. As Mike Simonsen, Founder of Altos Research, explains:

“. . . we’re seeing a more normal seasonal pattern now with inventory beginning to decline. We’re also seeing more home sellers withdrawing their listings to try again next year. In fact, for every two sales, there is another listing withdrawn from the market.”

But is that a smart move? While it might seem like a good idea to pull your listing too, here’s why that approach may not pay off this year.

Today’s Buyers Are Serious and Ready To Act

The biggest reason to stick with your plan to sell now is that the buyers who are looking at this time of year are serious about making a purchase.

They’ve been sitting on the sidelines for a while waiting for affordability to improve. And now that mortgage rates are down from their recent peak, they’re ready to make their move. Mortgage applications are rising – and that’s a leading indicator that buyers are preparing to jump back in. And since they’ve already put their needs on the back burner for so long, they’re even more eager than buyers usually are at this time of year.

These aren’t window shoppers. They’re highly motivated buyers who want to move fast – and that’s the kind of buyer you want to work with. As Freddie Macsays:

“During the fall months, serious homebuyers are eager to settle in to a new home before the holiday season ramps up and the winter weather begins.”

By keeping your home on the market, you increase the chances of attracting people who are truly ready to make a purchase.

Bottom Line

While some sellers are choosing to take their homes off the market, this really isn’t the best move. With serious buyers eager to purchase, this is a great time to sell your house. Let’s connect to make sure we’ve got a strategy in place to make it happen.

If you’re wondering what’s going on with home prices lately, you’re definitely not the only one. With so much information out there, it can be hard to figure out your next move.

As a buyer, you might be worried about paying more than you should. And if you’re thinking of selling, you might be concerned about not getting the price you’re aiming for.

So, here’s a quick breakdown to help clear things up and show you what’s really happening with prices—whether you’re thinking about buying or selling.

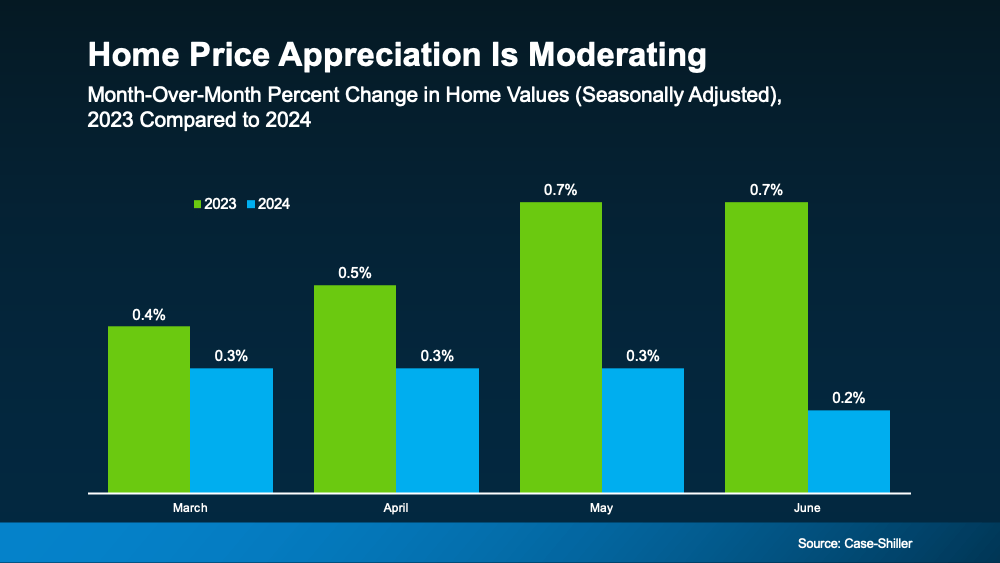

Home Price Growth Is Slowing, but Prices Aren’t Falling Nationally

Throughout the country, home price appreciation is moderating. What that means is, prices are still going up, but they’re not rising as quickly as they were in recent years. The graph below uses data from Case-Shiller to make the shift from 2023 to 2024 clear:

But rest assured, this doesn’t mean home prices are falling. In fact, all the bars in this graph show price growth. So, while you might hear talk of prices cooling, what that really means is they’re not climbing as fast as they were when they skyrocketed just a few years ago.

What’s Next for Home Prices? It’s All About Supply and Demand

You might be curious where prices will go from here. The answer depends on supply and demand, and it’s going to vary by local market.

Nationally, the number of homes for sale is going up, but there still aren’t enough of them to meet today’s buyer demand. That’s keeping upward pressure on prices – even though recent inventory growth has caused that home price appreciation to slow. Danielle Hale, Chief Economist at Realtor.com, said:

“. . . today’s low but quickly improving for-sale inventory has ushered in more market balance than would otherwise be expected . . . This should help home prices maintain a slower pace of growth.”

And here’s one other thing you may not have considered that could play a role in where prices go from here. Since experts say mortgage rates should continue to decline, it’s likely more buyers will re-enter the market in the months ahead. If demand picks back up, that could make prices climb a bit further.

Why You Should Work with a Local Real Estate Agent

While national trends give a big-picture view, real estate is always local – especially when it comes to prices. What’s happening in your neighborhood might be different from the national average based on what supply and demand look like in your market. That’s why it’s crucial to get local insights from a knowledgeable real estate agent.

As your go-to source for everything related to home prices, a local agent can provide the most current data and trends specific to your area.

So, if you’re planning to sell, they can help you price your house accurately. And when you’re ready to buy, they can find the right home that fits your budget and your needs.

Bottom Line

Home prices are still rising, just not as quickly as before. Whether you’re thinking about buying, selling, or just curious about what your house is worth, let’s connect so you have the personalized guidance you need.