If you’re wondering what’s going on with home prices lately, you’re definitely not the only one. With so much information out there, it can be hard to figure out your next move.

As a buyer, you might be worried about paying more than you should. And if you’re thinking of selling, you might be concerned about not getting the price you’re aiming for.

So, here’s a quick breakdown to help clear things up and show you what’s really happening with prices—whether you’re thinking about buying or selling.

Home Price Growth Is Slowing, but Prices Aren’t Falling Nationally

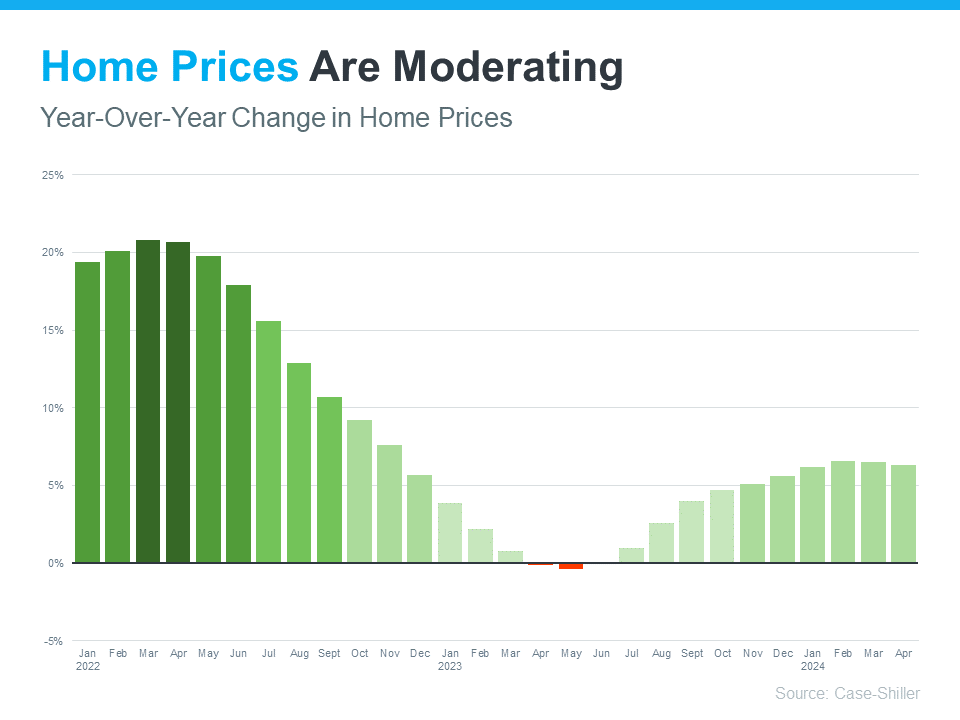

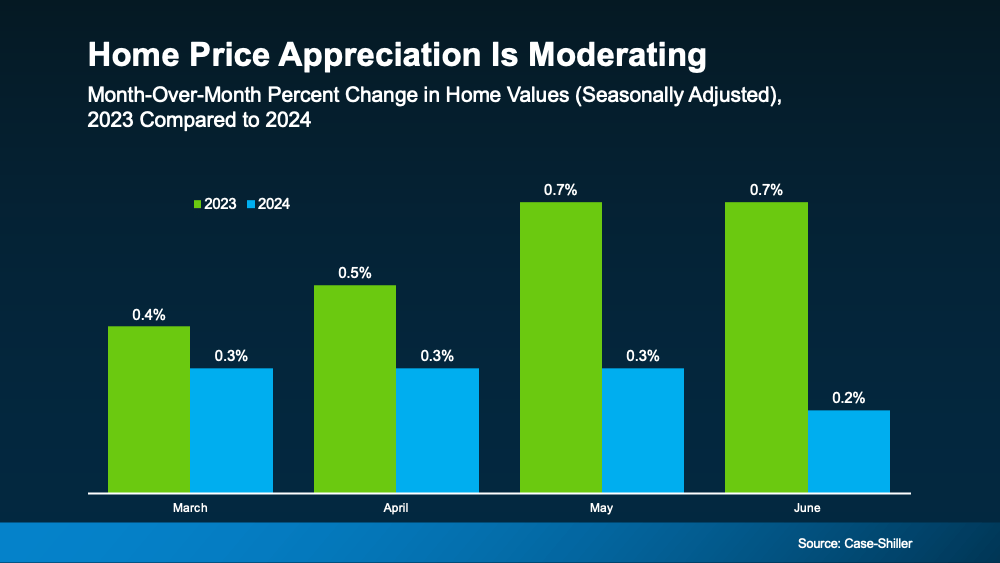

Throughout the country, home price appreciation is moderating. What that means is, prices are still going up, but they’re not rising as quickly as they were in recent years. The graph below uses data from Case-Shiller to make the shift from 2023 to 2024 clear:

But rest assured, this doesn’t mean home prices are falling. In fact, all the bars in this graph show price growth. So, while you might hear talk of prices cooling, what that really means is they’re not climbing as fast as they were when they skyrocketed just a few years ago.

What’s Next for Home Prices? It’s All About Supply and Demand

You might be curious where prices will go from here. The answer depends on supply and demand, and it’s going to vary by local market.

Nationally, the number of homes for sale is going up, but there still aren’t enough of them to meet today’s buyer demand. That’s keeping upward pressure on prices – even though recent inventory growth has caused that home price appreciation to slow. Danielle Hale, Chief Economist at Realtor.com, said:

“. . . today’s low but quickly improving for-sale inventory has ushered in more market balance than would otherwise be expected . . . This should help home prices maintain a slower pace of growth.”

And here’s one other thing you may not have considered that could play a role in where prices go from here. Since experts say mortgage rates should continue to decline, it’s likely more buyers will re-enter the market in the months ahead. If demand picks back up, that could make prices climb a bit further.

Why You Should Work with a Local Real Estate Agent

While national trends give a big-picture view, real estate is always local – especially when it comes to prices. What’s happening in your neighborhood might be different from the national average based on what supply and demand look like in your market. That’s why it’s crucial to get local insights from a knowledgeable real estate agent.

As your go-to source for everything related to home prices, a local agent can provide the most current data and trends specific to your area.

So, if you’re planning to sell, they can help you price your house accurately. And when you’re ready to buy, they can find the right home that fits your budget and your needs.

Bottom Line

Home prices are still rising, just not as quickly as before. Whether you’re thinking about buying, selling, or just curious about what your house is worth, let’s connect so you have the personalized guidance you need.